Bangladesh has fired the opening shot in its most ambitious battle against cash even as mounting cyber fraud threatens to undermine confidence in the country's rapidly expanding digital payments ecosystem.

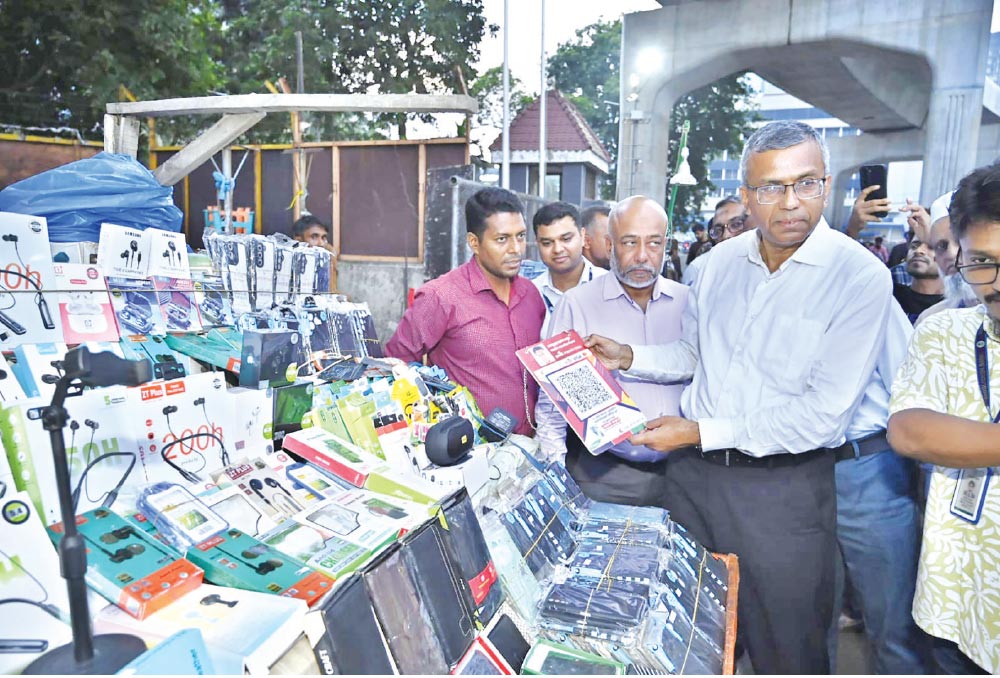

Last week, Bangladesh Bank Governor Md Mostaqur Rahman abandoned the formality of conference halls and boardrooms to make a modest purchase from a roadside stall in Dhaka using the newly introduced Bangla QR system.

Mobile financial services (MFS) operators say the message was unmistakable. “Rather than launching the initiative with another policy speech, the Governor chose to demonstrate that the country's digital transformation will succeed only when ordinary citizens�"not merely banks, fintech firms and large retailers�"embrace electronic payments as naturally as they now exchange banknotes”, said Major General (retd) Monirul Islam, of bKash Limited.

“It was a small transaction with far-reaching implications�"a carefully choreographed statement that Bangladesh's cashless revolution must begin where cash still dominates”, said a Bangladesh Bank official adding that a silent revolution is unfolding across Bangladesh's marketplaces with rising mobile money transactions.

The nationwide rollout of Bangla QR, the country's first mandatory interoperable QR payment platform, marks one of the boldest reforms of Bangladesh's retail payments landscape. From 1 July, every bank, MFS provider and payment service provider has been required to adopt the interoperable Bangla QR platform, allowing customers to pay any merchant instantly using a single QR code, irrespective of their bank or mobile payment application.

By bringing banks, mobile financial service (MFS) providers, payment service providers and merchants under a single digital payment standard, policymakers hope to loosen the grip of the cash economy, draw millions of informal businesses into the financial mainstream and accelerate the country's transition towards a transparent, efficient and inclusive digital economy.

“Bangladesh Bank intends to bring all 1,200 bank branches onto the platform within three months while onboarding at least 1.2 million users, creating one of the country's largest integrated digital payment networks”, said a top central bank official.

The initiative builds upon more than a decade of financial innovation since the launch of bKash in 2011, itself inspired by Kenya's groundbreaking M-Pesa. Mobile financial services have since transformed financial inclusion by connecting millions of previously unbanked people to formal financial services, making Bangladesh one of South Asia's fastest-growing digital payment markets.

Yet despite this remarkable progress, the country still trails India, whose Unified Payments Interface (UPI) has revolutionised retail payments, and Kenya, where mobile money has become woven into the fabric of everyday economic life.

Economists argue that the rewards of a truly interoperable QR ecosystem extend far beyond convenience. A less-cash economy could dramatically reduce the enormous costs of printingbanknotes, strengthen tax compliance, improve transparency, enhance monetary policy transmission and encourage millions of small enterprises to join the formal economy.

For roadside traders and micro-businesses, QR payments remove the need for costly point-of-sale terminals, democratising access to digital commerce.Yet beneath the promise of this digital revolution lies an uncomfortable reality.

The same technologies that are making payments faster, cheaper and more accessible are also opening new frontiers for organised cybercrime. As QR payments, mobile wallets and internet banking proliferate, fraudsters are exploiting fake QR codes, phishing attacks, cloned mobile applications, identity theft, account takeovers and increasingly sophisticated AI-driven impersonation scams to target unsuspecting consumers.

What was once hailed as one of Bangladesh's greatest achievements in financial inclusion is now becoming an increasingly attractive hunting ground for organised criminal networks.

Financial crime analysts estimate that scams linked to mobile financial services have siphoned off nearly Tk 21,000 crore over the years, exposing deep vulnerabilities within the country's digital financial architecture.

A recent study found that 6.3 per cent of individual MFS users and 17 per cent of MFS agents have already fallen victim to fraud, while digital payment platforms are increasingly being exploited for money laundering, online gambling and other illicit financial activities.

Investigators warn that criminal syndicates are deploying artificial intelligence, cloned caller identities, synthetic voice technology and sophisticated social engineering techniques capable of deceiving even financially literate customers.

The battlefield has shifted from physical theft to digital deception, where trust has become both the greatest asset and the easiest target. Therefore, experts say building a cashless economy is no longer simply about expanding digital infrastructure or increasing transaction volumes.

“It demands rigorous Know Your Customer (KYC) compliance, world-class cybersecurity, real-time fraud detection, stronger regulatory oversight and continuous public awareness. Without those safeguards, the digital revolution could lose the very public confidence upon which its success depends”, said a top banker working in a private commercial bank.

Ultimately, experts say, the success of Bangla QR will not be judged by the number of QR stickers displayed on shop counters or the value of electronic transactions processed each day. “It will be judged by whether consumers, merchants and businesses believe digital payments are safer, faster and more reliable than cash itself”.

Bangladesh has laid the foundations for a cashless future. Whether that future becomes reality will depend not only on technological innovation, but on the country's ability to stay one step ahead of increasingly sophisticated cybercriminals.