Just a few months ago, Bangladesh’s skincare groups turned into a full-blown theatre of sunscreen drama. Newsfeeds were flooded with photos and memes - hands held up to the camera, posing like victory, fingers streaked with product, captions pleading, “Will this much be enough?” Some women posted two shy, thread-thin lines of sunscreen along their fingers. Meanwhile others, in deliberate exaggeration, smothered both fingers so thickly that the cream looked like frosting.

It had all started with a single post, a screenshot of a follower’s hand, barely dotted with sunscreen. Above it, the group admin wrote, “My followers complain sunscreen doesn’t work. Meanwhile, this is the amount they use.” The joke spread in minutes. Yet beneath the laughter, those tiny lines of sunscreen made the follower look miserly in a way that was painfully familiar. The harsh truth is that - with the price of each tube, middle and lower income users quietly calculate how to stretch every drop, wondering if they can still “take care” of their skin while rationing the product to make it last one month more.

Right now, we live in a world where fashion supersedes many other basic needs of our day-to-day life. Our everyday life is influenced by beauty influencers, where we often strive to look like our idols in K-dramas. And in that pursuit, we often spend an enormous amount of money on cosmetics to look the best that we can.

The global cosmetics industry has grown into one of the most powerful and resilient market sectors in the world. Cosmetics, including skincare, haircare, makeup, fragrances, and toiletries, account for one of the largest segments of modern consumer goods.

With an annual value exceeding USD 420-450 billion, the cosmetics business has transformed from a luxury-oriented market to a competitive global industry. Growth rates of this industry remain steady at 4-6% annually, driven by rising disposable income, urbanization, rise of e-commerce, and expanding male grooming trends.

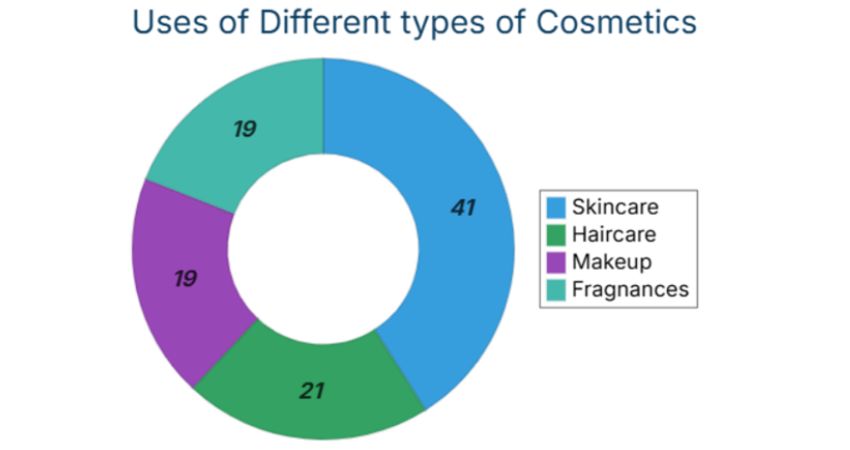

Skincare remains the dominant category, accounting for over 41% of total global revenue. Makeup represents around 19%, haircare approximately 21%, and fragrances about 19%.

Bangladesh’s domestic cosmetics and toiletries market has expanded sharply over the last two decades. Industry surveys estimate the market value at roughly Tk 50,000 crore, equivalent to around USD 5-6 billion. A young population, rising middle-class purchasing power, and high demand for beauty products among women and increasingly among men contribute to this rapidly growing consumer base.

However, Bangladesh is still heavily import-dependent. The country imports USD 200–300 million per year in finished cosmetics. Hundreds of millions more in raw materials such as fragrance oils, emulsifiers, packaging components, and chemicals. China is the largest source of these imports.

But when it comes to China, it’s clear that we’re not the only ones buying cosmetics from them. China rose as a cosmetics powerhouse beside its already thriving tech and day-to-day trivial products.

The Chinese cosmetics market was valued at USD 69.4 billion in 2023. Within a decade, this figure is likely to surpass USD 100 billion by economists. China’s rise is closely tied to a strong domestic manufacturing base. Recent estimates show that China accounts for approximately 23.4% of the global cosmetics market, making it one of the largest, if not the largest national cosmetics industry in the world.

Now the question arises: does Bangladesh really lack its own cosmetics manufacturing industry? The answer is more complicated than a simple yes or no.

At the level of everyday body care, the country actually has several long-running local players. Square Toiletries’ Meril line and companies like Kohinoor Chemical (brands such as Tibet, Sandalina) produce a full range of personal-care products. From basic skincare items to toiletries, which are specifically formulated for Bangladeshi consumers and climate. Alongside these, there are brands occupying a more “conscious” or “natural” space such as, Aarong Earth, selling face packs, scrubs, handmade soaps etc.

Social media is also crowded with small pages selling ubtan-style masks, herbal soaps and oil blends that promise “chemical-free” care rather than the lab-heavy formulas associated with K-beauty or Japanese skincare.

However, most of these “old-guard” brands focus on soaps, lotions and simple skin- and hair-care, not on large-scale color cosmetics. The kind of mass-produced makeup lines that define aspiration for many urban consumers such as foundations, concealers, eyeshadow palettes and long-wear lipsticks in the style of Lakmé or Maybelline - are still dominated by foreign brands, either imported or marketed locally through distributors.

When it comes to makeup, however, it is not entirely true that Bangladesh has “no brands at all.” We do have locally anchored names – but with the complication that in many cases the branding and retail network sit in Bangladesh while the actual manufacturing is outsourced abroad, or vice versa, making it hard to claim cleanly “home-grown, made-here” color cosmetics in the way we talk about pharmaceuticals.

Lilac, for example, is a mid-range skincare line whose serums, face washes, scrubs and tinted lip balms are widely sold on Bangladeshi platforms like Shajgoj, Rokomari and other e-commerce sites. Listings describe dermatologically tested formulations targeting issues like hyperpigmentation, dark spots and sensitivity, and some products list France as the country of Lily produces mass-market color cosmetics and personal-care items; the brand is owned by Remark LLC USA but its products are manufactured in Bangladesh and distributed nationwide through Herlan Store. Ethereal by S focuses on handcrafted lip-care products such as lip oils, balms, tints and liners, produced in small batches in Bangladesh under a licensed setup. Nirvana Color offers a full range of affordable color cosmetics including foundations, lipsticks, powders, eye products and nail enamels, marketed as Bangladeshi.

Despite a growing demand for beauty products, Bangladesh has not yet been able to build a fully “Made in Bangladesh” cosmetics industry in the way it has done with pharmaceuticals or garments.

But why can't we meet the needs of our own population? The first and foremost barrier is the lack of adequate infrastructure. To produce even a small batch of product, an advanced cosmetic manufacturing process is needed, which requires formulation labs, stability testing, toxicology screening, and even trained cosmetic chemists, which in our country are quite scarce.

Secondly, regulations for the distribution of authentic products are weak and fragmented. The absence of clear, strictly enforced standards allows counterfeit and low-quality products to flood the market. This even leads to discouraging serious investment in high-end local production.

Finally, consumer psychology could also play the most evident role in our society, the persistent belief that “foreign means better.” Until regulatory clarity, technical expertise, and consumer trust evolve together, fully domestic cosmetics production will remain an aspiration rather than a reality.

But there are certainly hopes for us. Bangladesh’s experience in sectors like ready-made garments (RMG) and pharmaceuticals demonstrates that we can become globally competitive when manufacturing ecosystems are developed strategically. The cosmetics industry, though different in nature, shares certain features with these sectors: relatively low capital entry barriers, labor-intensive processes, and strong export potential.

We already have several advantages if we decide to manufacture cosmetics on large scales. Our low production costs, large workforce, access to regional markets and a strong RMG sector experience in packaging, branding, and global compliance. Growing demand for beauty products means that we already have our customer base. We already have the demand, now we just need to supply the goods.

If Bangladesh as a whole invests in manufacturing, product formulation, certification, and branding, the country can not only reduce its import dependence but also position itself as an exporter within Asia.

Based on the report published by BBS Health and Morbidity Status Survey (HMSS) 2025, an average of 37.23 out of every 1,000 people suffer from skin diseases. More than 1,500 patients receive treatment every day at the dermatology outpatient department of Dhaka Medical College Hospital.

According to dermatologists, 30-45% of all dermatology visits are related to unhygienic low quality cosmetics. Cosmetics are among the top 5 causes of contact dermatitis. 20-30% of adult acne cases worsen due to cosmetics. 10–20% of facial fungal infections are cosmetic-related. 1 in 3 patients has a condition that is caused or worsened by cosmetic use.

These can be traced to fake or adulterated cosmetic products. At the same time, many imported formulations fail to perform under Bangladesh’s humid, polluted climate or align with local skin tones. Together, these realities do not indicate the rejection of global beauty brands, but to the urgent need for locally developed and regulated cosmetics that are tested on Bangladeshi skin and produced with clinical accountability.

-The writers are students of the Department of Mass Communication and Journalism, University of Dhaka